Since the new year began, my investing portfolio is looking rather basic and boring – and I love it! If you happened upon my last post on tax loss harvesting, you know that towards the end of 2022 I unloaded my position in a lot of hand-picked stocks (where I was in the red) to offset some taxes I was going to be paying from a real estate syndication that cashed out late last year. Truth be told, I have a slight degree of remorse about selling off the several hundreds of shares of Tesla that I owned – as it has rebounded/recovered rather quickly since then. Regardless, essentially, I have nothing but a couple of index funds (i.e. VTI and VXF) and a couple of stocks (i.e. COST and BRK.B) remaining that I stayed profitable in. In that simplicity, I have found I have a lot less stress about the going ons in the market day-to-day, and I feel strongly resolved to stay this course and filter out the noise and temptations of following grifters that make promises of higher returns and unfathomable riches.

As of writing this post, the current rate of inflation in the United States is a 6.4%. Taking on some degree of risk is essential if we hope to grow our money in a way that combats the toll inflation takes on our hard earned dollars. I first learned about the concept of ‘uncompensated risk‘ on the White Coat Investor blog. Basically he says that when we make an investment, a compensated risk will provide us a reasonable expected (but not guaranteed) return. However, in an uncompensated risk scenario, we take on additional risk without an increase (and in many cases, a decrease) in the generated returns.

I do not profess to be an expert at any of this. A disclaimer that I consistently make is to consult professionals for financial advice, as I am a mere pediatric dentist that is trying to figure out his footing on the path to financial independence. I have tripped and stumbled countless times along the way, and fallen flat on my face (e.g. Celsius and the whole crypto fiasco) in many instances as well.

There is a lot that goes into investing that I really only know a small (more like minute) fraction about. Lots of economic indicators and trends to look at e.g. jobs reports and unemployment, consumer confidence indices (CCI), etc. Changes in interest rates, geopolitical events, and macroeconomic factors (e.g. inflation, recession) drive the markets performance. Savvy investors have all kinds of sophisticated software to give them real-time market data, research reports, and analytical tools. And for those people that have the time to commit, the advanced training and education, along with the temperament to endure the volatile nature of the stock market day-to-day; more power to them.

For anyone average like myself; who work for a living, limited hours in the day to commit to much else, just trying to set aside some kind of nest egg for the future – taking on uncompensated risk investments really can be quite a dangerous setback. The key is diversification in your portfolio of investments. I hope we all know by now never to put all your eggs in one basket. The one saving grace for me has been that all my ‘speculative’ investing has been limited to 5-10% of my overall portfolio. My crazy crypto experience with Celsius Network (where potentially I stand to lose everything), my uncertain venture into real estate syndications (which fortunately has partially and profitably paid out) – it’s all been a bit of a wash, but I cap it all within a small percentage of my total asset allocation.

“Invest in what you know…and nothing more.”

Warren Buffet

For those that have read my blog, one of my previous posts talks about my love for watching some late night comedy bits to start my day. There was an interview recently on The Daily Show where Hasan Minhaj debated Kevin O’Leary (from Shark Tank) and essentially called him out on being a (paid) spokesperson for the recently failed FTX crypto exchange. About midway through the interview, Minhaj makes the point (around the 17:45 min mark) that most retail investors would be better off investing in boring Vanguard S&P 500 index funds versus trying to time the market and chase the trends that influencers make us believe was their formula for success. It resonates with me on a personal level since I so foolishly followed the same preaching’s of a similar conman by the name of Alex Mashinsky of the Celsius Network. The other point being that social media nowadays has made it so (dangerously) easy for grifters giving the illusion that millions can be made effortlessly simply by doing as they do.

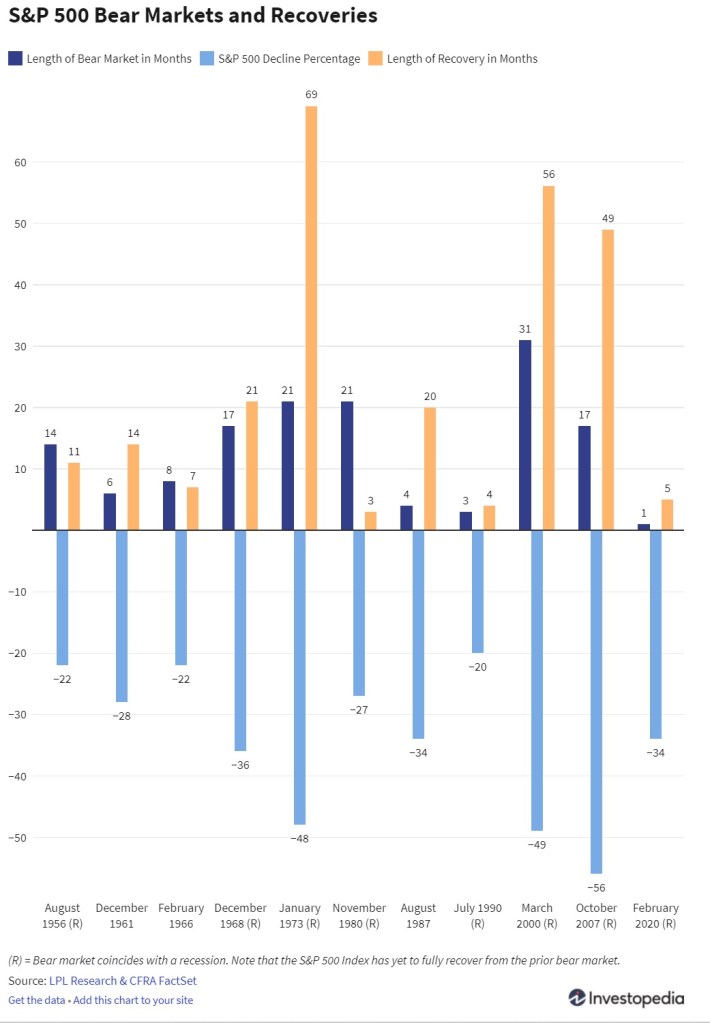

The performance of the U.S. stock market overall, dating back to the 1920s, has provided an annualized average return of around 11.88% since its 1957 inception (according to Investopedia). After factoring in inflation, it runs somewhere around the 8-9%. That’s pretty darn good. If we put money into any one stock its the equivalent of putting it all on black (my attempt at a roulette metaphor in case you missed it) – that is uncompensated risk. I am willing to designate a small piece of that to certain companies and real estate deals (preferably REITs) that I think may, in the long-term, be worthwhile; but a vast majority of my investing endeavors from here on out will be in the slow and steady S&P500 index funds.

Wishing you all the best in your journey! Thank you all for visiting this site and spending some time to read through this post!