If this blog affords me anything, it is the opportunity to write about the things that occupy my attention. Day after day, since 2022 started, I wearily watch as the stock market plummets and any profits and gains from the last several years get wiped out within a matter of months. Like the gray, rainy weather in Seattle that leads some to experience seasonal affective disorder (SAD); so to can the chronic red and sharp declines in the stock market lead to gloom and mental anguish.

By definition, a correction is a market decline that is more than 10%, but less than 20% off of a recent market high. A bear market is usually defined as a decline of 20% or greater. The S&P 500 index is the overall representation of the market’s performance. There are plenty of other terms (i.e. market dip, crash, etc.) that are pertinent but could just as easily be Investopedia‘d.

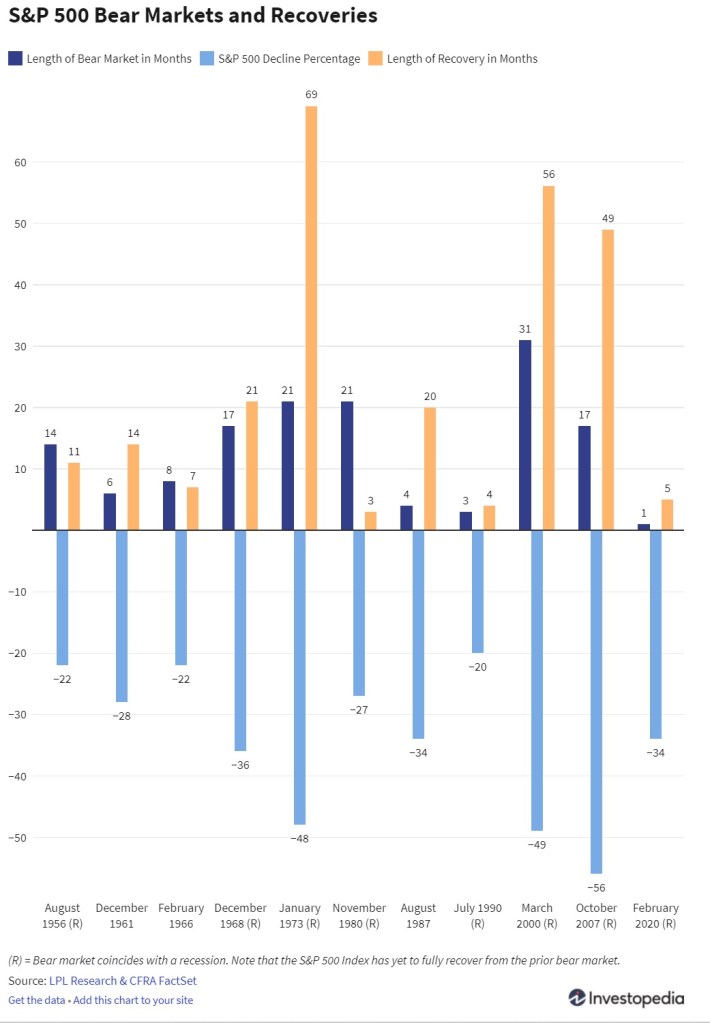

Again, graphs like the one above present the performance of the overall S&P 500 Index. If you are like me, and your portfolio is a composite of index funds, stocks and bonds, and other asset classes – you may fare significantly better, catastrophically worse, or somewhere in-between.

Individual stocks are prone to much more volatility. A character on an HBO show rides his Peloton, suffers a heart-attack and dies – causing the stock to sink nearly 12% the next trading day. A large group of traders on the r/WallStreetBets Reddit forum helped drive GameStop’s stock surging up over 400% once upon a time. A misinterpreted tweet by Elon Musk stating to ‘use Signal’ confused investors and sent the wrong stock up soaring over 6300%.

More recently it is the Ukraine and Russia conflict and the question of an impending war? The Federal Reserve and possibility of several interest rate hikes? Certainly economy-related concerns but also lots of other miscellaneous events and outside influences can spook investors and cause the fear that lead to sharp market declines and panic selling.

Probably a totally irrational skepticism on my part – but I think the news media has manipulation tactics and selectively seeds content, stock analysts have their own obvious biases and agenda, and of course corrupt politicians have access to insider information that allow them the ability to execute privileged and personally advantageous trades. It is hard to find trustworthy sources to believe. Just my opinion.

In a past blog, I briefly introduced a bit about my investing approach. Certainly trying times like these test our conviction. Lots of different investment philosophies exist – each with their own strengths and weaknesses. I subscribe to a philosophy known as Dollar-Cost Averaging (DCA). You can read about it a bit more here, but essentially you put same amount of money in the same stock (or index fund, etc.) on a regular basis over time, regardless of the share price.

“Our favorite holding period is forever.”

– Warren Buffett

In terms of personal investing, the February-March 2020 bear market was the only one I have actually had to endure. Before that, I was dirt broke and too busy suffering through dental school and multiple residency programs. Even though I know many others are experiencing these same tribulations right now, there is a unexplainable loneliness and depression that sets in when you see these steep market declines. I used Vanguard’s financial advisor services for a short while, and while I ultimately decided to stop and take things into my own hands, I did appreciate that I was not constantly worrying about how the markets were doing.

I dare not try and predict where the bottom of this latest market crash will be. However, I find some solace in knowing, if we stay the course and weather this storm, the market will do what it historically has – deliver some dependable returns.

In a future post, I will go over a few other investment strategies I do to minimize risk, including: invest in syndication real estate deals, invest in REITs and rental properties, and more recently – dare I say it – cryptocurrencies. Diversification is the name of the game!?

As always, thank you for taking the time to read through this post. Hope that some of this information can be useful to you, and please feel free to share in your own experiences!